A Future Where AI is Building, But No One is Buying | The Take 22/10/25

As gaming becomes an increasingly specialist market, saving money is only one side of the coin.

Greetings to The Take, our editorial issues of the AI and Games Newsletter where we dig into the bigger issues impacting artificial intelligence in the video games industry. Issues of The Take are exclusive to premium subscribers of AI and Games.

Hello one and all, and welcome to this edition of The Take. We’re but a couple of weeks away from running our very own AI and Games Conference, and I had originally planned a Researcher’s Digest issue for this week, but the recent conversation surrounding gaming purchase patterns paints an interesting picture. Of a games industry largely propped up by hyper enthusiast buyers, where fewer players are buying new games, and it got me thinking about the narratives surrounding generative AI, and how it will help speed up production.

Follow AI and Games on: BlueSky | YouTube | LinkedIn | TikTok

As we’ve been told in various creative industries, the untapped potential of using (generative) AI is that it will yield all sorts of value for creators. It will allow us to make games faster, it will allow us to build richer and more complex experiences, that it will give even increase the number of jobs in these sectors. All of this leading to an implication that by bringing product to market faster, those products are yielding a greater return on investment due to the cost-savings AI can provide.

While I have a lot of grievances with these narratives - I agree with parts of it, while the rest is naïve posturing and speculation - that isn’t really my focus right now. If anything it’s the part I emphasised in the paragraph above. That this AI-powered nirvana will lead to more profit, given we’re making games more cheaply, and they’re going out to consumers faster.

But the recent data shared by market research firm Circana, suggests that the consumer market isn’t there for this kind of explosion of production. The games industry is already in a difficult space right now courtesy of global economics and other factors. If anything it only cements that AI is not the solution to these market trends. AI is often held aloft as this silver bullet that will make game development ‘cheaper’, creating “more games studios which should, therefore, mean more jobs” in the process. But that’s only one side of the coin, and it strikes me that lessons have not been learned from recent years of collective failure.

So in this episode of The Take, let’s get into:

How the ‘hyper enthusiast’ market props up the entire games industry.

How data from market research continues to paint an ugly picture of the health of the industry.

A failure to acknowledge the growing rate of production exceeds consumer habits.

AI being proposed as the silver bullet for game dev costs has no empirical basis.

The real risk that AI brings in escalating the race to the bottom.

This issue of The Take, like last month’s, is available in full to our premium subscribers! Please consider signing up to help support me and my team and allow us to continue to do this on the regular!

Consumer’s Gaming Habits

If you’re sitting there rather confused, let me build up a short primer for you. A couple weeks back the gaming press got worked up a bit by results from a research survey by Mat Piscatella and his team at Circana on video game purchase habits - all of which is part of Circana’s quarterly ‘future of games’ reporting.

The long and short of it, is “approximately a third of video game players purchase a new videogame less often than once per year, while about 36% of purchase a new game once a quarter or with higher frequency”.

The results of this survey are all the more damning when you begin to dig into the details:

Less than 15% of all consumers buy one game a month.

Only 55% of consumers are buying more than one game a year.

33% of players don’t buy games annually.

Now I can tell you straight away I fall in to that “more often than once a month” bracket. I am very much a ‘hyper enthusiast’. Naturally a big part of this is while our AI and Games newsletter has me reporting on the state of the industry, I am also a content creator who makes videos about games, and critically I play a lot of games in order to stay on top of the conversation. When suddenly Ball X Pit or Absolum are the games people are talking about in the moment, I am often playing those games both out of a desire to enjoy them, but equally I spend a lot of my time trying to figure what makes a game tick - be it technically, aesthetically, or otherwise. Could it be the next episode of our Artifacts or AI and Games video series?

[Both of those games are really good BT Dubs]

But also sometimes, heaven forbid, I just want to play a new game - and I have the money to do that.

Now if you heard about this story, or in fact if you’re reading this newsletter, odds are you fall under the same category. You’re interested in the video games industry, you’re interested in video games, you probably play video games. That puts you in a bracket that isn’t reflective of the bulk of the gaming populace. People play games, sure, but they maybe have one or two games they visit on the regular, and that’s about it.

Old Narratives No Longer Hold

In fact for the longest time it was argued that most gamers only buy a couple of titles a year, and it was assumed that was the annual entry of the Activision’s Call of Duty, as well as one big sports title. Naturally if you’re in the US, that’s Madden NFL though for the rest of the world it’s FIFA/EA Sports FC.

This idea was reinforced back in 2023 when Microsoft sought to appeal the UK’s Competition & Market’s Authority decision to try and block the proposed buyout of Activision/Blizzard, by presenting survey data that showed - among many other things - that the top two franchises for PlayStation gamers in Europe were FIFA [EA Sports FC] (33%), and Call of Duty (17%) in that order. The data also highlighted that the latter of the two would not force a significant number of players to change platform should it become Xbox exclusive. Funny reading that now when you realise how all the more dependant Microsoft has become on PlayStation sales of the franchise, but I digress.

But the Circana survey implies that even this is no longer holding true. That if more than a third of gamers aren’t even buying one game a year, are they moving the direction of only picking up every other Call of Duty? Or are happy to stick with their annual sports release until it has a bigger, more meaningful content update a year or two later?

The results not only reinforce this change of buying habits, but also it helps strengthen another narrative we started seeing last year, of people playing older games for longer.

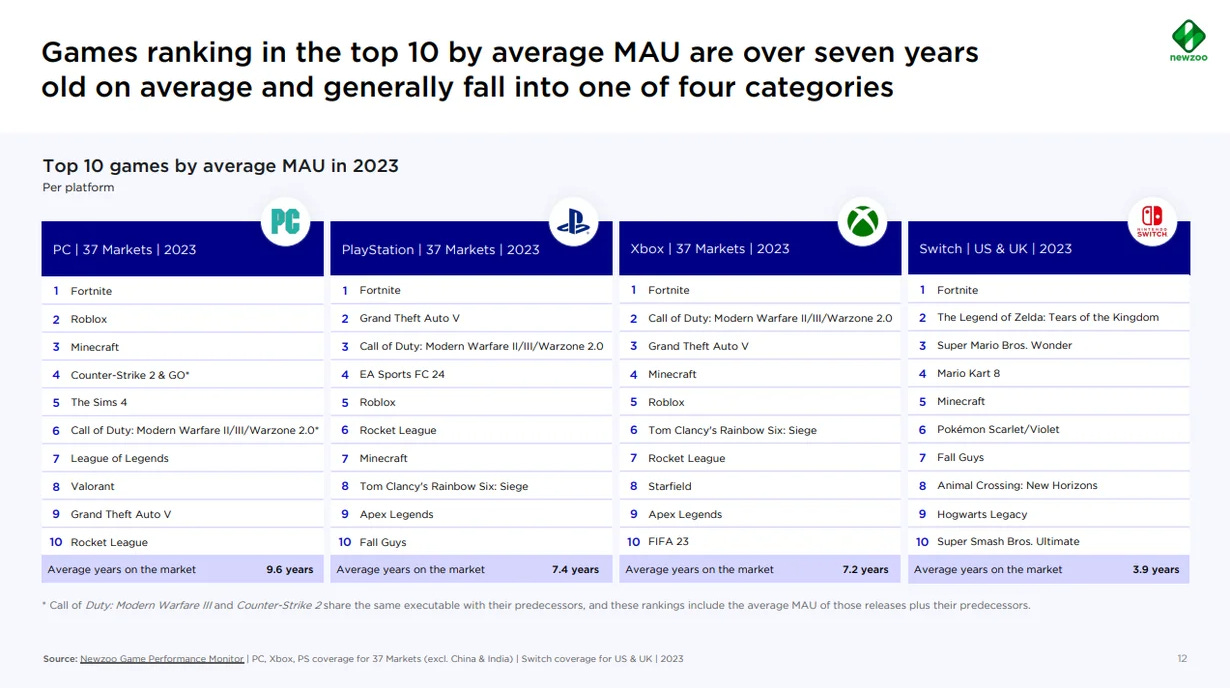

A NewZoo gaming report from the spring of 2024 added fuel to the fire of people sticking with existing games by highlighting that Monthly Active Users (MAU) for most active games in the US on PC, PlayStation and Xbox in 2023 were from titles that were on average 7 years old, or older. Adding to this issue was that new games in 2023 only accounted for around 8% of total playtime, with the latest entry in the Diablo franchise taking top billing.

Supply vs Demand

Per Circana’s own research, it’s estimated that around 75% of all US adults now play video games. But what games they play, and how much they spend on them has been an ongoing source of concern. All of this adds to an ongoing trend that has emerged in recent years:

People are not buying new games at the rates they have historically

(Some) Live service games and platforms are successfully retaining and monetising their audience.

While this one survey alone cannot be treated as 100% reflective of the trends throughout the gaming market, with Piscatella himself acknowledging that the sample for the survey was around 2500 US based gamers over the age of 13 (which is still sufficient to get a meaningful result), it reinforces an emerging narrative: people are not buying games at the rate consummate to development.

In other words: we’re making more games than people are buying.

This has, in a roundabout fashion, been seen to some extent with the horrid number of layoffs the industry has faced in recent years. As many a project - many of them live service - was commissioned during the heydays of players being on gaming platforms during the COVID pandemic and the variety of lockdowns that ensued. Ever since then there’s been a collective failure to acknowledge that while the gaming audience is larger than it’s ever been, the appetite to spend money on new and recurring content is not what it once was. The Epyllion report from back in January highlights that the bulk of gamers are in mobile - a space replete with casual recurring user spending - while PC is now in 2nd place as consoles struggle to retain market share.

We’ve seen many a AAA title fail spectacularly in recent years, all the while the hyper enthusiast audience is being pushed towards indie games, with thousands of them hitting Steam on an annual basis. A trend that is ever increasing, all the while the disposable income of the most avid of players continues to be tight as everything from global conflict to tariff’s and poor fiscal policy continues to have its impact.

All of this is leading to the fallacy that is often presented as fact: that (generative) AI is the solution to the games industry’s woes.

“Reduce the Cost of Making Games”

Returning to the my earlier point of how (generative) AI will make games cheaper, and easier to make. As we know this is an argument regularly made by studio execs and otherwise. In fact it was a leading argument by a trade representative when I was interviewed for an article on the BBC back in 2023 (shout out to Stefan Powell for chatting with me). Now if you read this article, I’m the one erring on the side of caution. Meanwhile Guy Gadney is plugging his work at Charisma.ai, but as I say it was the trade representatives that gave me the ick. TIGA’s Richard Wilson was quoted as saying “Reducing the overall cost of development will mean more games studios which should, therefore, mean more jobs.”

Now this point comes up again, and again, and again, whether it’s in creative industries like film, games, even civil service and government. When we talk about the potential for (generative) AI. It’s often about how it’s going to help save money, it’s going to create new jobs, and it may even lead to an improvement of product.

Now for one I have yet to see any empirical data that shows that the adoption of AI has led to a clearly definable saving in cost for game development. Naturally for generative AI we won’t see that for a few years until studios attempt to go that route and ship product - even if it burns bridges with consumers in the process. But even after a decade of the games industry using machine learning in production for everything from animation blending to cheat detection and texture upscaling, I’ve yet to see any studio come forward and say with any clear evidence that the adoption of AI saved them a percentage point of the anticipated budget. More often than not it leads to an improvement in quality, to handling increased scale, or it leads to increased throughput, but I’ve not see any studio seriously evaluate the efficacy of AI in context of historical budgets.

But let’s just say, for the sake of argument, that this proves to be the case. I would genuinely love to see us find ways to make games in a more cost effective way while retaining the levels of quality we’ve seen thus far. I really would, and I do think some cost savings are attainable. But quite often these expectations are somewhat fantastical in nature, and so I figure for this segment I want to believe in them hypothetically, just so I can raise an all important question:

If AI helps us speed up production, and ship games faster, who is going to buy them?

It’s a Two-Sided Relationship

There seems to be an assumption that by magically reducing the cost of development, it will mean there is a market more ready and willing to consume the product. But the data is really not lining up with this assertion.

The games industry has a problem right now of making too many games, and there isn’t a market big enough to consume everything that is coming out. Much like other forms of media, the vast majority of content receives very little exposure as social media aggregates and homogenesis the conversation such that even the enthusiasts are all talking about one or two specific titles during a particular window.

This has really stuck out to me a couple of times this year when both the AAA and indie gaming spheres struggled with scheduling launches. First with GTA VI looming over the AAA calendar - to a point that as I said in January, there was little announced in the back half of the year at that time. Meanwhile just a few weeks ago, indie titles moved dates around because of Hollow Knight: Silksong.

It does not strike me that we exist in a healthy industry where a single game - regardless of quality - can dominate the conversation.

Now of course if the costs are lowered courtesy of AI, it does mean that there is greater opportunity to bounce back from failure, and get another game up and running. But again, I ask, just how much revenue are you going to need, and if games are coming out 2x/3x/4x faster, you have two problems:

Can you guarantee that any of these games get market penetration?

Do consumers care? Or just go back to Fortnite?

AI is Not Your Silver Bullet

As I’ve discussed in my visits to everyone from Devcom to Pocket Gamer Connect, I continue to see people hold AI aloft as the silver bullet that will fix their problems. As I intimated just last week, I feel like we frequently try to use AI as a means to obfuscate the problem. Rather than address the real issues that sit at the route of the sector, we’re going to *waves hands* use a magical technology to address the problems that exist.

We’re slowly crawling our way back from the aftershocks of COVID, where a boom in revenue saw a collapse in the industry more broadly as expenditure increased only for revenue to decrease. Not drastically, but enough for many a studio or otherwise to reconsider their spending at a time that economies in the US and Europe are still struggling with a number of challenges - many self-inflicted, others brought upon them. Leading to a desperate clutch at potential Saudi cash despite the broader political implications - as we saw all too readily with EA just a few weeks ago.

The economic course correction of recent years has meant that games now cost more than ever - both to make, and to buy - and it seems perfectly timed that AI comes along as the potential solution. But at the end of the day, even if this works, it’s only one half of the problem. We need to get consumers to buy the games. But if they don’t have the cash to spare, or are opposed to the adoption of AI on principle, will those cost savings really have been worthwhile?

While I mentioned mobile gaming earlier in the article, one of the reasons the aforementioned enthusiast crowd often ignores it is the poor quality. Many a mobile title is thrown together quickly hoping to catch the attention of players, only moving on to the next. Is this the future of the PC/console market? As studios burn through AI-assistend projects more readily hoping to get eyeballs in an ever fractured userbase.

I guess I can look on the bright side. Buying a couple games a month means I have a pretty decent sized backlog to work through when I begin to lose interest...